The Fed Is Beginning to Run Like a Corporation

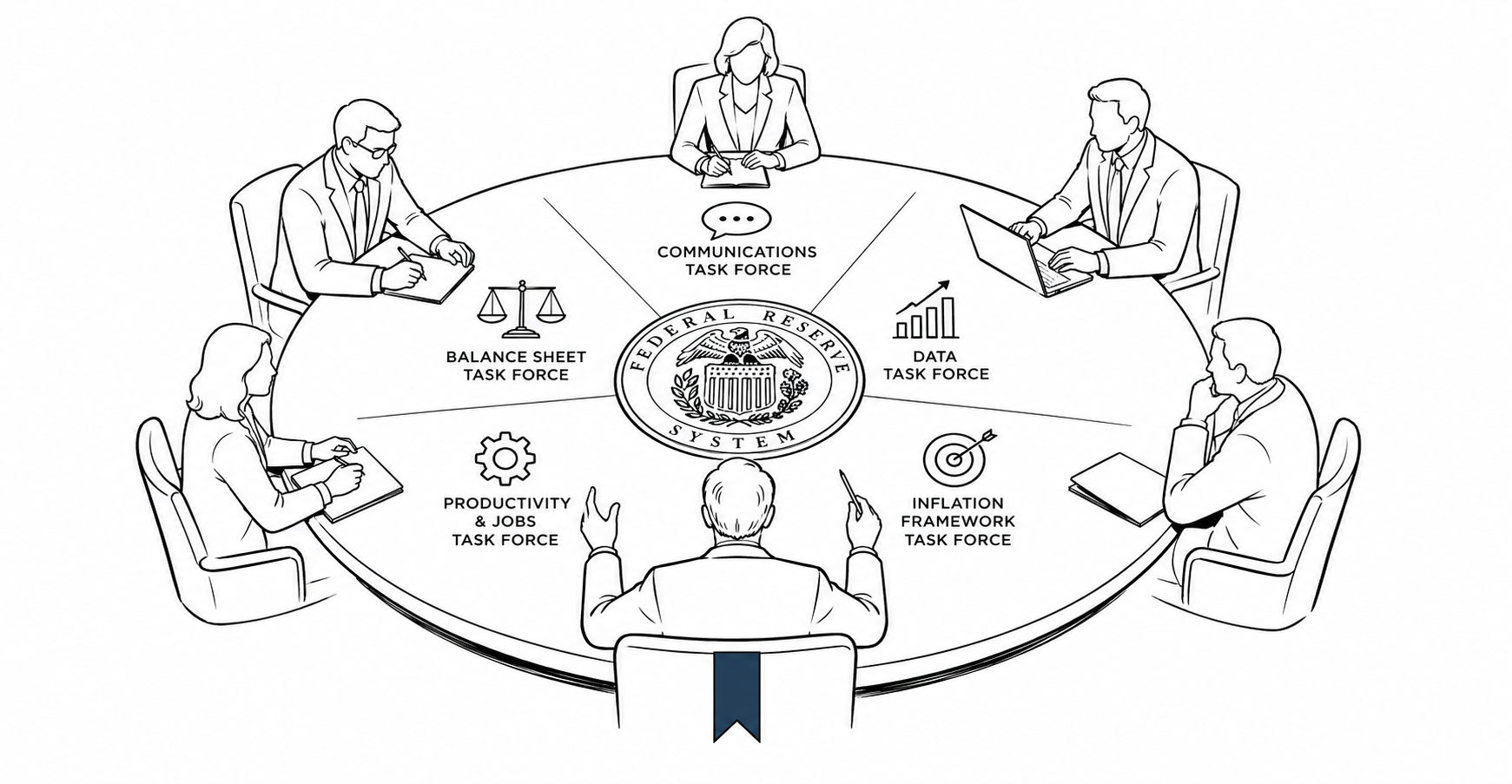

Kevin Warsh has been chair of the Federal Reserve for less than a year, and his first major move is not a rate change. It is an org chart.

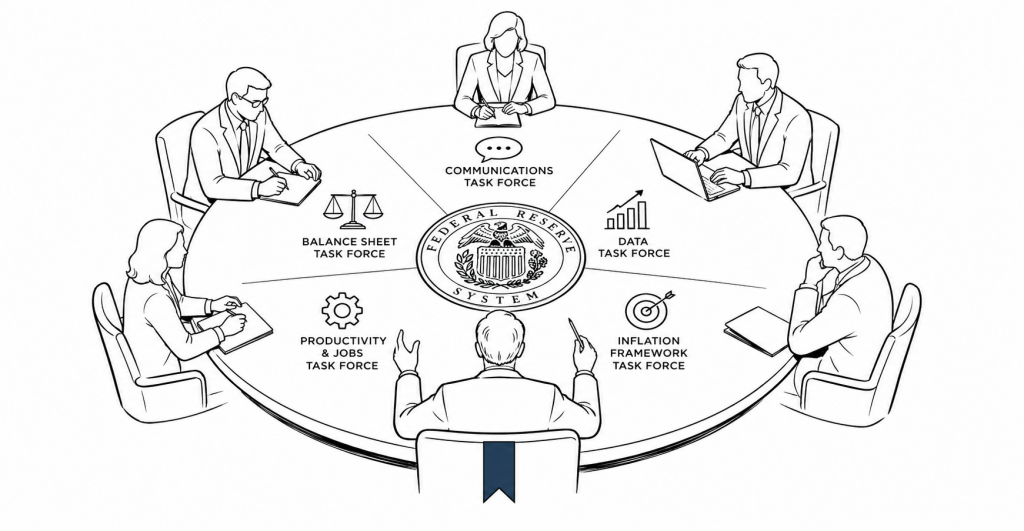

Warsh announced five task forces this week covering communications, the balance sheet, data, productivity and jobs, and the Fed’s inflation framework. Each pairs internal staff with outside experts — selected by Warsh. None delivers immediate policy changes. All of them deliver something else: a structured process through which Warsh’s preferences can become the institution’s conclusions.

The $6.7 trillion balance sheet task force is the most watched. The Fed accumulated that position through a decade of quantitative easing and pandemic-era intervention, and it has been the source of ongoing debate about whether the Fed has become too embedded in financial markets to function as an independent monetary authority. Warsh has long believed the balance sheet needs to shrink. A task force that “reviews the benefits and risks” of the current approach — staffed partly by experts Warsh selects — is designed to produce a report that the full Federal Open Market Committee will find harder to ignore than Warsh’s personal views alone.

The communications task force is the subtler signal. A vote on changes is deferred until the task force reports, late this year. That deferral covers the press conferences, the meeting transcripts, the forward guidance architecture — all of the public-facing machinery through which markets read the Fed’s intentions. Whoever shapes the communications review shapes how the institution talks about itself, which is how institutions change without changing their stated mandate.

This is recognizably a CEO’s playbook. You enter a complex institution, identify the levers, build a structured process that generates legitimacy for the conclusions you already hold, and let the timeline do the work. The approach is not illegitimate. It is, in fact, how most durable institutional change happens — through process rather than edict. What it means for monetary policy is that the Fed’s next chapter will be written by task forces, not rate decisions, and the reports will arrive over the next six to twelve months.

The open question is what happens when a task force recommends something the FOMC majority doesn’t want to do. Warsh’s tool is legitimacy, not authority. If the process produces conclusions that clear political cover for the changes he wants, the playbook worked. If it produces reports that the committee reads and then sets aside, the institution will have spent a year reviewing itself without changing — which is also an outcome, and also a signal about where the Fed’s internal politics actually sit.

— SSC Business Desk | Social Storytellers Collective