Private Label Is Eating Brand Loyalty. The Consumers Driving It Are Not Who Retailers Expected.

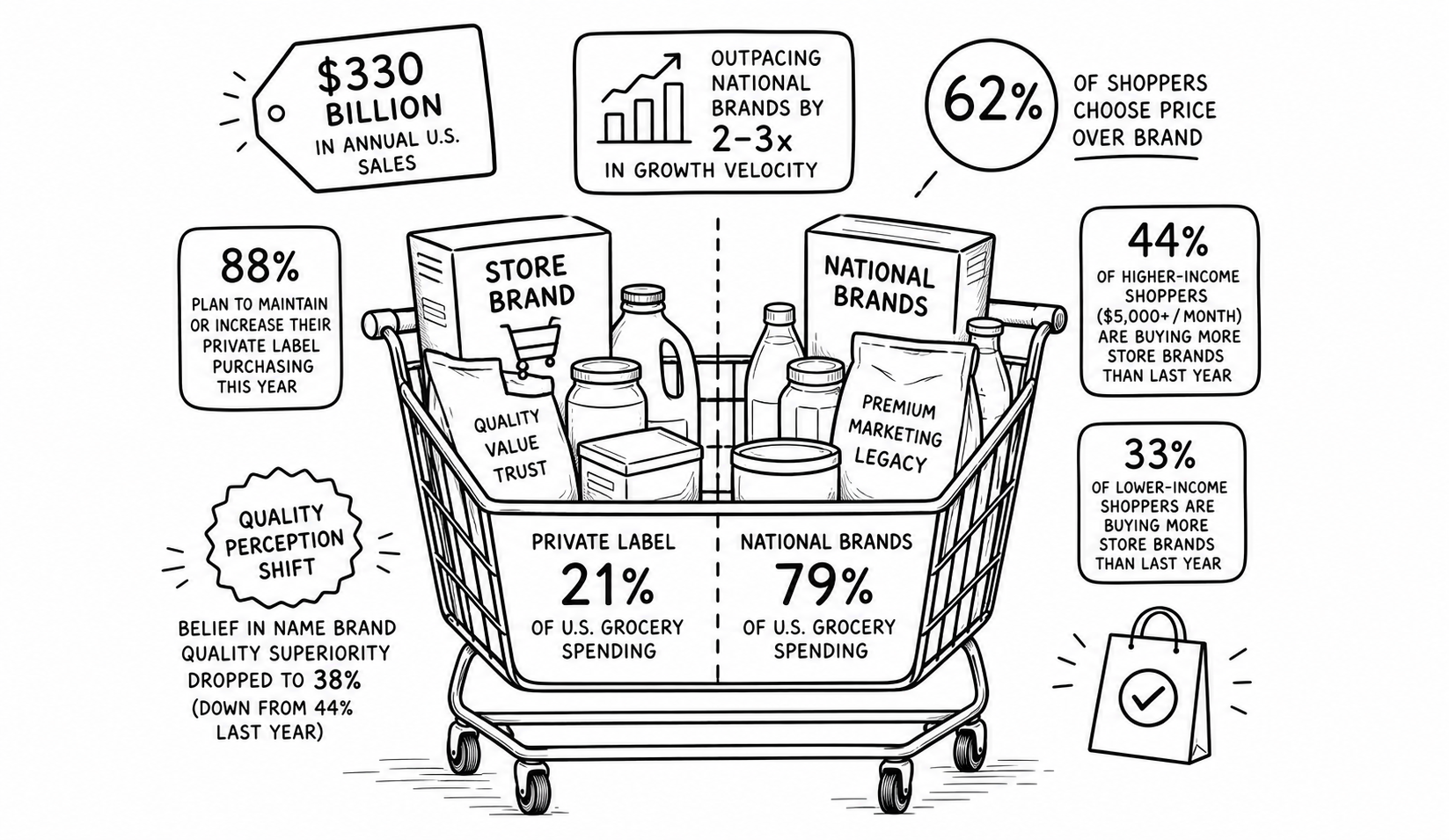

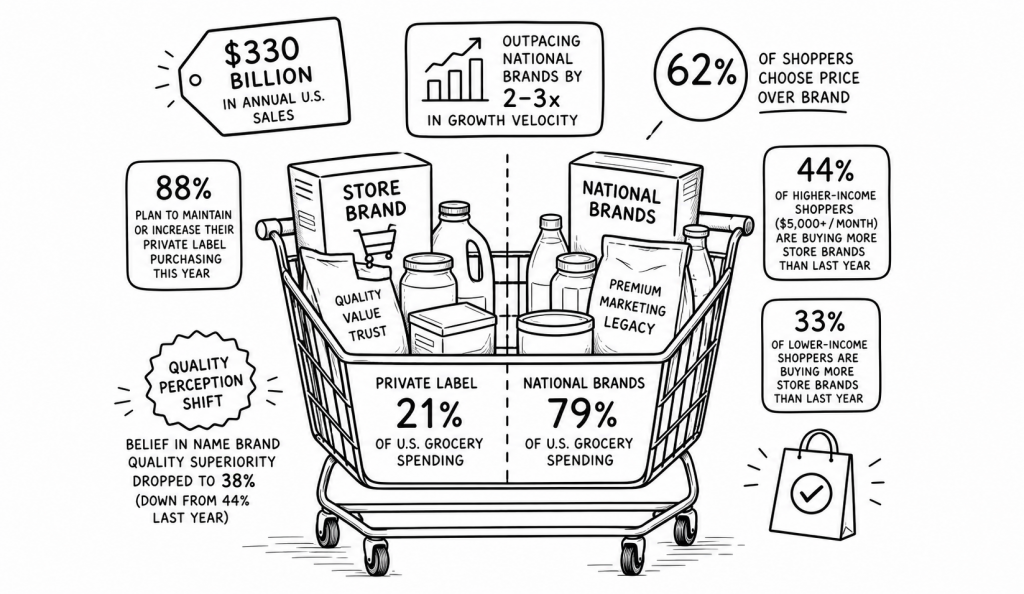

Private label now accounts for $330 billion in annual U.S. sales, with a 21% share of all grocery spending. Store brands are outpacing national CPG brands by 2 to 3 times in growth velocity. 62% of shoppers now choose price over brand when making purchase decisions, according to Ibotta’s 2026 State of Spend report, which surveyed more than 5,000 grocery shoppers. 88% plan to maintain or increase their private label purchasing this year. Those are the numbers retailers have been watching. The number they weren’t expecting is this one: 44% of higher-income shoppers — those earning $5,000 or more per month — are buying more store brands than last year. Among lower-income shoppers, that figure is 33%.

The conventional story about private label growth is a pressure story. Inflation hits, budgets tighten, consumers trade down from the brand they preferred to the store brand they can afford, and national brands wait for the cycle to end and the loyalty to return. That story has been true in previous cycles. The Ibotta data suggests something different is happening in this one. The shoppers substituting at the highest rate are not the ones under the most financial pressure. They are the ones with the most discretion — and they are using that discretion to leave.

The mechanism is not complex. National brands built loyalty on a premium justified by two things: perceived quality and the weight of marketing investment that made the brand feel like a signal of something. Private labels competed on price because they couldn’t compete on the second thing, and for years the first thing was close enough that the premium held. What has changed is that private label quality has closed the gap on the first thing while the second thing has weakened. The Ibotta report found that belief in name brand quality superiority dropped to 38% this year, down from 44% last year. Consumer trust in private label quality is now at 61% in food and 60% in home products. When quality perception equalizes, the premium becomes indefensible.

Kirkland Signature, Costco’s private label, generated $90 billion in sales in 2025 — more than Procter & Gamble’s Tide, Unilever’s Dove, and ConAgra’s entire brand portfolio combined. Trader Joe’s carries private label on more than 80% of its products, at premium prices, with loyalty that national brands spend billions in marketing to approximate. These are not budget substitutes. They are preferred brands that happen to be owned by the retailer. The premium private label segment — Tesco Finest, Sainsbury’s Taste the Difference, Costco Kirkland — is growing three to four times faster than value private label. The consumers buying premium store brands are not trading down. They are choosing differently.

What national brands are losing is not market share in the traditional sense — a temporary dip that reverses when conditions change. They are losing the premise. Brand loyalty was always built on the assumption that consumers couldn’t reliably judge quality on their own and needed the brand as a proxy. Private labels have spent the past decade proving that the proxy is no longer necessary. 42% of U.S. consumers now buy private label predominantly or exclusively. The question for every national brand that has spent decades building a premium on perceived quality is the same: if a shopper with options and income is choosing the store brand and staying there, what does the national brand actually own?

— SSC Business Desk | Social Storytellers Collective