Wage Growth Is Running Below Inflation Again. The Jobs Report Called It Healthy.

The numbers are real. So is the gap between what they measure and what workers are experiencing.

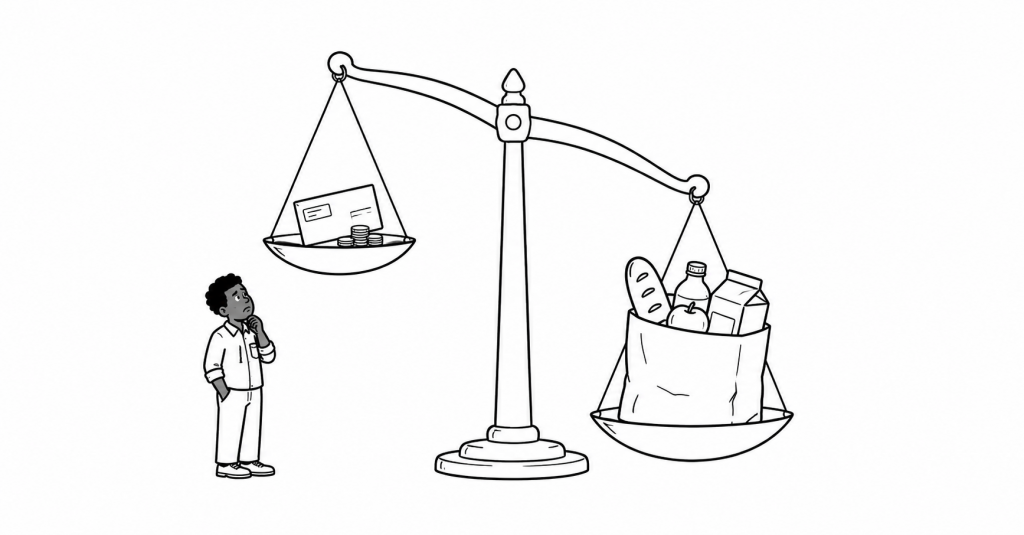

The Bureau of Labor Statistics released the May 2026 employment situation on June 5. The headline was strong: 172,000 jobs added, unemployment unchanged at 4.3%, prior months revised upward by a combined 93,000. The BLS also released its real earnings data the same week. Real average hourly earnings decreased 0.7% from May 2025 to May 2026. Average hourly wages rose 3.4% in nominal terms over the year. Consumer prices rose 3.8% over the same period. The workers adding jobs to the payroll are earning less in real terms than they were a year ago.

This gap is not incidental to how the labor market is performing. It is the labor market’s performance, measured for workers rather than employers. The jobs report headline reflects what the economy produced. The real earnings data reflects what workers received from that production. These are different numbers measuring different things, and they keep moving in different directions. Elise Gould, senior economist at the Economic Policy Institute, noted in a June 5 social media breakdown of the report that given recent trends, real wages would very likely continue to fall, making it increasingly difficult for workers and their families to make ends meet.

The sector picture inside the May report sharpens the aggregate. Financial activities employment fell by 22,000 in May and is down 107,000 since a peak in May 2025. The tech sector has shed 0.7% of employment since 2023. Job gains concentrated in leisure and hospitality, local government, and health care — sectors with structurally lower wages than the sectors losing workers. That is not merely a compositional quirk. It is a description of where the economy is growing and who is capturing the gains. A leisure and hospitality job is not the same economic unit as a financial services job. The headline job count does not distinguish between them.

Labor economist Aaron Sojourner told The National News Desk that inflated energy prices, policy uncertainty from tariffs and immigration enforcement, and technological uncertainty from AI are all producing what he described as a deer-in-the-headlights effect among employers — unwilling to move, unsure what is coming. The result is a labor market that looks stable from the outside and feels precarious from the inside: low layoffs, low quits, low hiring, low real wage growth. The quits rate, the best indicator of worker confidence, stayed essentially flat in April. Workers are not quitting because they do not feel they have better options, not because they are satisfied where they are.

The Federal Reserve is watching the same numbers and drawing the opposite policy conclusion. A 172,000 headline makes rate cuts less likely, not more. For workers, that means borrowing costs stay elevated, housing affordability stays constrained, and the purchasing power erosion documented in the real earnings data continues without a monetary policy response designed to reverse it. A jobs report can be both technically strong and materially inadequate for the people it counts. May 2026 was both.