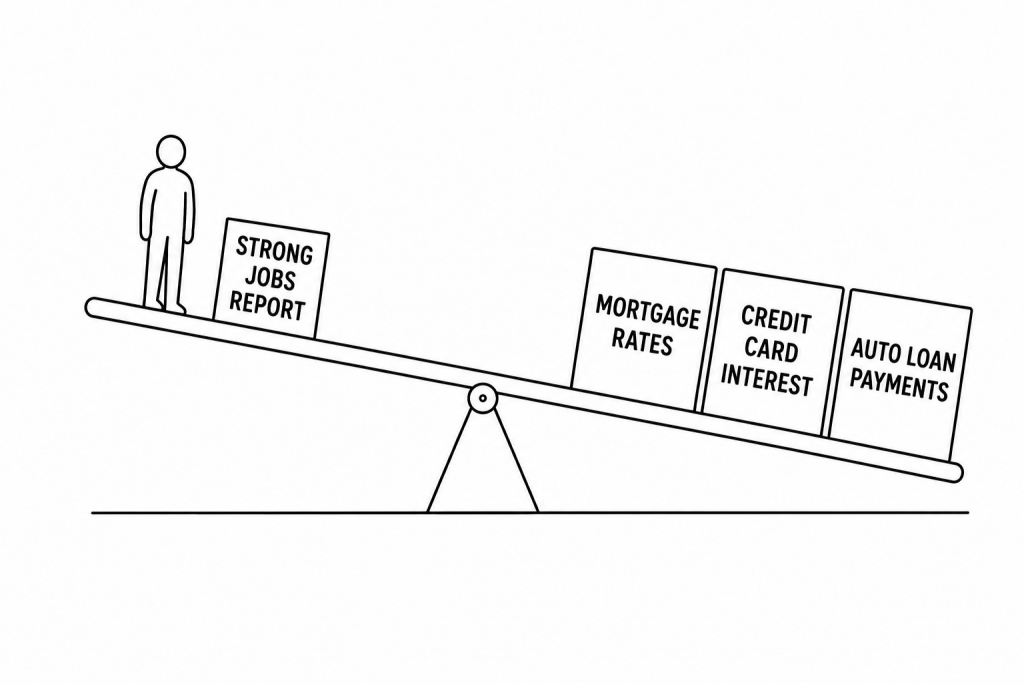

A healthy labor market is reassuring investors. It may also be keeping mortgages, credit cards, and auto loans more expensive for everyone else.

Stronger-than-expected U.S. employment data this week increased market expectations that the Federal Reserve could keep interest rates elevated for longer than many investors had anticipated, according to Reuters. March and April payroll figures were revised upward by a combined 93,000 jobs, reinforcing the view that the labor market remains resilient despite broader concerns about economic slowing. For workers, that sounds like good news. For households carrying debt, it may mean waiting even longer for borrowing costs to fall.

The tension reflects a growing contradiction inside the American economy. Strong hiring has traditionally been treated as an unambiguous sign of economic health — more people working means more income, more consumer spending, and greater financial stability. Yet in an economy shaped by inflation concerns and aggressive interest-rate policy, strong employment numbers can produce an entirely different outcome. Evidence that workers remain employed can reduce pressure on the Federal Reserve to lower rates.

That matters because interest rates now influence nearly every major household financial decision. The 30-year fixed mortgage rate is averaging approximately 6.5 percent this week, according to Freddie Mac, Bankrate, and Zillow — down from nearly 8 percent in October 2023 but still more than double the historic low of 2.65 percent reached in January 2021. The result is a market where 82.8 percent of homeowners with a mortgage already hold a rate below 6 percent, per Redfin — locked into their existing homes, unable or unwilling to sell into a market where their next mortgage would cost significantly more. That lock-in effect suppresses housing supply and keeps prices elevated even as rates edge lower. Auto loans have become more expensive. Credit card balances are carrying higher interest charges. When markets interpret strong labor data as a reason for the Federal Reserve to maintain tighter monetary policy, economic strength in one area translates into financial pressure somewhere else.

The connection to small business is where the contradiction sharpens. This week’s jobs report showed small businesses accounting for 67,000 of the 122,000 private sector jobs added in May — the single largest contributor to May’s headline number. Those same small businesses are financing operations, equipment, and inventory in an environment where borrowing costs remain elevated. As SSC reported today in When Brisket Costs More Than the Business Can Bear, the small business owners producing the labor market’s headline strength are simultaneously absorbing input costs and financing conditions that the headline number was never designed to reflect. Strong hiring data is being generated by the same businesses that tight monetary policy is making harder to sustain.

Americans increasingly experience the economy through different lenses. A worker who keeps a job, receives a raise, or sees employers continue hiring may view the economy as stable. That same worker may simultaneously face higher monthly payments, more expensive financing, and reduced access to homeownership. As SSC reported in The Inflation Story Isn’t About Prices Anymore, credit cards are increasingly functioning as a bridge between stagnant purchasing power and rising living expenses — not fueling consumption but preserving continuity. The strong jobs report and the rising credit card balance are both real. They are not describing the same household financial reality. The metrics and the lived experience are not always measuring the same thing.

Policymakers, economists, and financial markets often focus on employment growth because it remains one of the clearest measures of economic resilience. Households tend to focus on affordability. A strong jobs report may reassure Wall Street while doing little to lower the cost of buying a house, financing a vehicle, or carrying existing debt.

The American economy is increasingly rewarding labor market strength while penalizing debt exposure. Households with stable employment and substantial assets may benefit from the current environment. Households relying on borrowed money to purchase homes, build businesses, or manage everyday expenses face a different reality. As long as employment remains strong and inflation concerns linger, good economic news may continue arriving with a higher monthly payment attached.